Salesforce Cognitive DevOps Market Projected to Reach $3.23B by 2031

At SalesforceDevops.net, we’ve conducted a rigorous analysis of how AI-powered Virtual Employees (VEs) are reshaping the Salesforce services landscape. Our latest market sizing research suggests a significant growth trajectory for this emerging technology category, with the Cognitive DevOps market projected to reach $3.23 billion by 2031. This represents an 6.3% penetration of the serviceable available market.

Perhaps most revealing in our analysis is the striking 20x disparity between the Salesforce DevOps software market (around $250M) and the corresponding Salesforce DevOps services market subject to AI reinvention (over $5B). This ratio appears to be more than a Salesforce-specific observation. This observation potentially represents a new rule-of-thumb across enterprise software ecosystems, where implementation, integration, and ongoing management services consistently dwarf the underlying software expenditure.

This software-to-services multiplier provides a crucial lens for identifying where AI disruption potential is highest, as Virtual Employees are poised to automate substantial portions of these service-heavy domains while maintaining quality standards. For investors and strategists, these service-heavy segments represent the most fertile ground for AI-driven transformation.

Table of contents

- What is a Virtual Employee (VE)?

- What is Cognitive DevOps?

- Understanding TAM, SAM, and SOM

- Customer Segmentation and Service Multipliers

- Segment-Specific Adoption Trajectories

- Technology Maturation Effects

- Salesforce Ecosystem Growth Moderation

- Comparative Benchmarking

- VE SOM (Revenue) Model

- Salesforce VE SOM (Revenue) Estimate

- Market Dynamics: Forces That Could Reshape the Trajectory

- Why These Numbers Matter

- What’s Next?

- Cognitive DevOps Players to Watch

What is a Virtual Employee (VE)?

A Virtual Employee is an autonomous or semi-autonomous AI agent that performs work traditionally done by a human knowledge worker. In the Salesforce context, this means writing Apex or Flow, configuring Data Cloud mappings, providing advisory services, pushing releases through a pipeline, or triaging support cases—24/7, API-native, and at effectively infinite scale. VEs aren’t just “bots”; they possess memory of prior actions, can reason across multiple systems, and plug into collaboration channels (Slack, email, ticket queues) as first-class teammates.

What is Cognitive DevOps?

Cognitive DevOps is the discipline of embedding those Virtual Employees directly into the software delivery lifecycle—planning, build, test, release, and run—so that every step is continuously optimized by machine reasoning. Think of it as DevOps 3.0: CI/CD pipelines augmented by LLM-powered code reviewers, metadata diff engines that self-heal, and monitoring agents that remediate issues before a human ever sees an alert. The goal isn’t just faster releases; it’s an exponential improvement in cognitive throughput—the amount of product and configuration insight an organization can push into production per dollar.

Understanding TAM, SAM, and SOM

Before diving into our numbers, let’s clarify three key terms:

- Total Addressable Market (TAM): The overall revenue opportunity available if a service or product could reach 100% market penetration without constraints. Calculating TAM for AI-driven services today is inherently challenging due to the vast scale and complexity involved. Virtually all current spending on human labor—amounting to trillions of dollars globally—could theoretically become part of this market as automation and AI technologies advance, highlighting both immense potential and substantial uncertainty. For those reasons, we choose to not estimate VE TAMs in this bottom-up analysis.

- Serviceable Available Market (SAM): The segment of the TAM realistically targeted by products or services given current market constraints and technologies. In this case, we seek the amount of current external services expenditures that could be targeted by a VE service provider.

- Serviceable Obtainable Market (SOM): The realistic portion of the SAM that companies can capture within a specific timeframe, given factors like competition, adoption rates, and resource limitations. This number represents industry SOM for VE sales in Cognitive DevOps.

Our estimates focus primarily on SAM and SOM to give investors and entrepreneurs actionable insights into strategic planning.

Customer Segmentation and Service Multipliers

We began by analyzing Salesforce’s FY2025 customer base, categorizing organizations into six tiers based on annual license spend: from large enterprises (3XL, >$10M) to small businesses (S, <$50K). For each segment, we calculated ancillary service multipliers (ranging from 3.3x for 3XL enterprises to 0.38x for S-tier customers) based on extensive partner interviews, anonymized invoice samples, and customer validation.

This segmentation provided the foundation for estimating the total ancillary services market across DevOps, implementation, maintenance, migration, and security service categories. The model reveals a $81.0 billion ancillary services market executed alongside Salesforce’s $35.7 billion services and subscription business in fiscal year 2025, which ended January 31, 2025.

This analysis counts only billable consulting, implementation, and ongoing managed services attached to Salesforce subscriptions. It excludes AppExchange ISV revenue, additional cloud infrastructure spending, and the downstream business revenue IDC adds to its ‘Salesforce Economy’ figures.

Segment-Specific Adoption Trajectories

We identified four major categories of services which allows us to segment VE SOM (Revenue). Rather than applying uniform adoption rates across all service categories, we calibrated distinct penetration curves reflecting the unique characteristics of each segment:

- DevOps services (11% adoption by 2031): The highest adoption potential due to standardized processes and established automation practices

- Implementation & Maintenance (8-9% by 2031): Moderate adoption reflecting greater variability in customer requirements

- Migration services (5.5% by 2031): Lower adoption due to data governance considerations and validation requirements

- Security services (3% by 2031): The most conservative projection, acknowledging regulatory constraints and risk sensitivities

These segment-specific trajectories represent the reality that automation potential varies considerably across service categories.

Technology Maturation Effects

Our model incorporates increasing efficiency gains over time by escalating the “VE discount” percentages annually. For example, the DevOps automation discount rises from 50% in 2025 to 60% by 2030, reflecting anticipated improvements in AI model capabilities, process standardization, and integration efficiencies.

This approach acknowledges that early-generation AI solutions will not immediately achieve maximum labor substitution but will steadily improve their displacement capabilities as the technology matures.

Salesforce Ecosystem Growth Moderation

Rather than projecting constant growth in the underlying Salesforce market, we implemented a tapering trajectory from 9% in 2025 to 6.25% by 2031. This deceleration reflects platform maturation, the law of large numbers, potential market saturation in certain segments, and macroeconomic considerations.

Comparative Benchmarking

To validate our projections, we benchmarked adoption curves against comparable enterprise technology rollouts such as:

- Cloud infrastructure adoption (2010-2020)

- DevOps tooling penetration (2015-2022)

- AI-enhanced productivity applications (2022-2025)

In each case, initial adoption typically proceeds at 0.1-0.3% per year during the pioneering phase, before accelerating to 1-3% annual increases as organizational comfort and implementation patterns standardize.

VE SOM (Revenue) Model

The following table illustrates how we arrived at these baseline figures for 2025. The VE Target SAM represents what Salesforce customers currently spend with outside contractors to perform the services within each sector. The Discount Rate column is the discount on the target revenue received by the VE vendor in 2025. Multiplying the VE Target SAM with the Discount Rate yields the VE Discounted SAM. Next, we use our model to predict the Adoption Rate for each sector in the specified fiscal year. The Adoption Rate is then multiplied by the VE Discounted SAM to give us the forecasted VE SOM (Revenue).

| VE Target Sector 2025 (Millions) | VE Target SAM | Discount Rate | VE Discounted SAM | Adoption Rate | VE SOM (Revenue) |

| DevOps & Release Engineering | $11,464 | 50% | $5,732 | 0.05% | $2.9 |

| Implementation & Integration | $14,839 | 40% | $8,903 | 0.03% | $1.8 |

| Managed Services / Ongoing Admin | $6,701 | 60% | $2,680 | 0.03% | $1.2 |

| Consulting / Change Management | $13,243 | 35% | $8,608 | 0.03% | $1.4 |

| Security & Compliance | $4,922 | 30% | $3,446 | 0.01% | $0.4 |

| Total VE Target SAM | $51,169 | ||||

| Total VE Discounted SAM | $29,369 | ||||

| TOTAL VE SOM (Revenue) | $7.7 |

The VE‑Target SAM is the $51 billion subset of the broader $81 billion Salesforce ancillary‑services pool that is directly addressable by Cognitive DevOps Virtual Employees—after stripping out categories such as AppExchange ISV fees, infrastructure charges, and low‑touch support work that fall outside near‑term VE automation scope.

Salesforce VE SOM (Revenue) Estimate

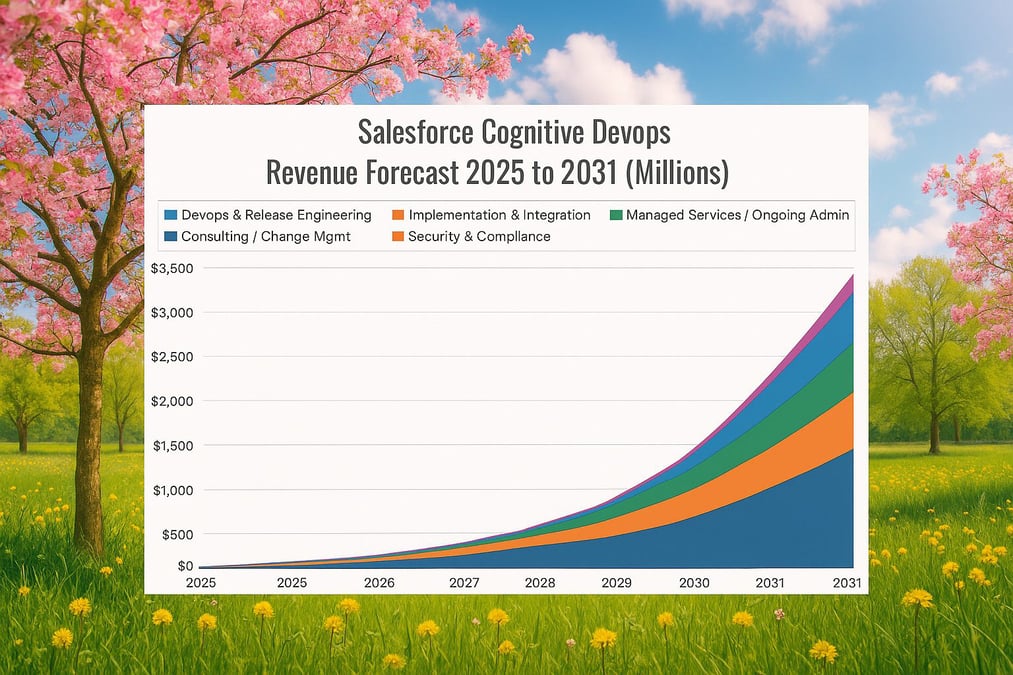

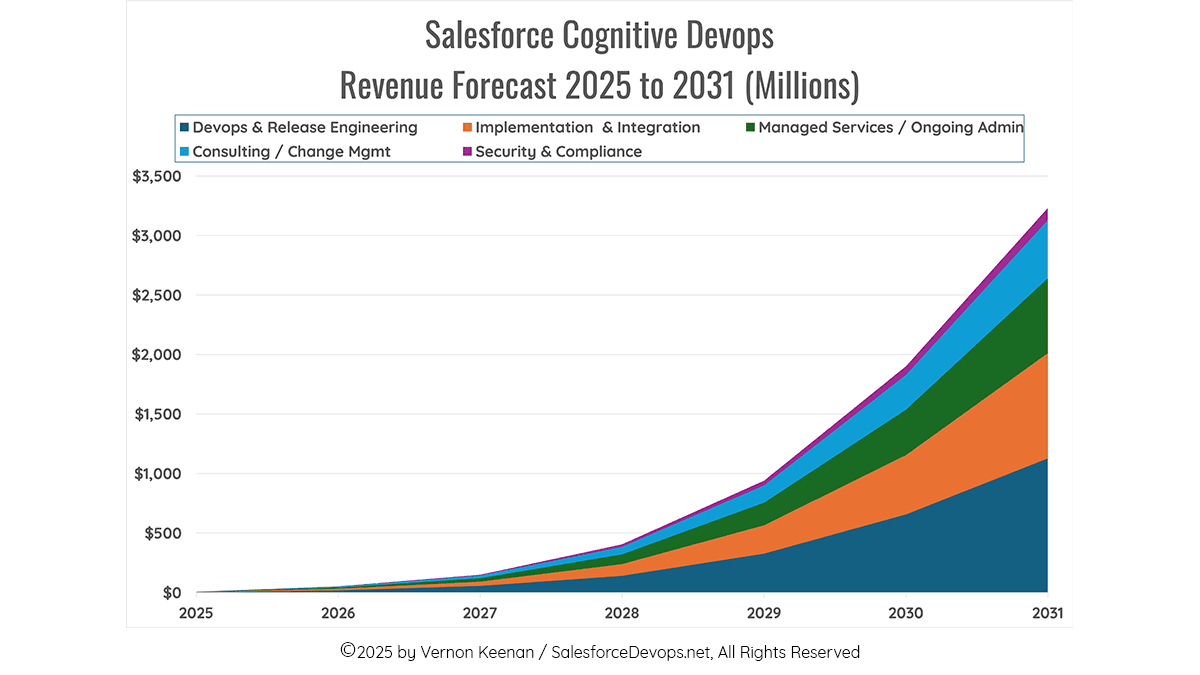

Applying a similar methodology across a 5-year projection of Salesforce sector revenue provides guidance on future revenue. Our conservative SOM projections through FY2031 account for historical enterprise technology adoption patterns, integration challenges, and organizational barriers. We forecast $52 million in VE-related sales in FY2026, growing to $3.23 billion by FY2031.

| Forecast VE SOM (Revenue, Millions) | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 |

| DevOps & Release Engineering | $2.9 | $19 | $55 | $140 | $327 | $656 | $1,127 |

| Implementation & Integration | $1.8 | $13 | $36 | $99 | $239 | $499 | $884 |

| Managed Services / Ongoing Admin | $1.2 | $11 | $29 | $81 | $189 | $382 | $629 |

| Consulting / Change Management | $1.4 | $8 | $23 | $65 | $146 | $293 | $488 |

| Security & Compliance | $0.4 | $2 | $7 | $20 | $39 | $72 | $103 |

| TOTAL VE SOM (Revenue) | $7.7 | $52 | $150 | $406 | $940 | $1,902 | $3,232 |

These numbers represent a conservative estimate of the revenue that Cognitive DevOps companies and entrepreneurs might achieve, acknowledging enterprise procurement cycles, governance requirements, integration complexities, and organizational change management challenges.

Market Dynamics: Forces That Could Reshape the Trajectory

While our conservative projection provides a grounded baseline for strategic planning, several market forces could significantly alter this trajectory.

Potential Headwinds

Compute Resource Constraints: The explosive growth in AI model training and inference has already strained global GPU supply chains. AI-related compute demand growth could create bottlenecks that limit scalability of Cognitive DevOps platforms and raise operational costs.

Regulatory Uncertainty: The regulatory landscape for AI systems remains in flux. New compliance requirements could slow adoption, particularly in heavily regulated industries like financial services and healthcare – sectors that represent substantial portions of the Salesforce customer base.

Channel Disruption: Traditional Global Systems Integrators (GSIs) will likely mount defensive responses to protect their margins, potentially including aggressive acquisitions of emerging Cognitive DevOps startups that could constrain innovation and pricing competition.

Acceleration Catalysts

The Widening Intelligence Gradient: As early-adopter organizations demonstrate measurable advantages in deployment speed and cost efficiency, competitive pressures could accelerate adoption beyond our 6.3% penetration rate in the 2031 projection.

Cognitive Commoditization Effects: Initial data from AI-native consultancies indicates they’re achieving 30-40% cost advantages while maintaining or improving quality metrics. If these trends continue, market adoption could accelerate as financial incentives overcome organizational inertia.

Self-Reinforcing Innovation Cycles: There’s potential for a virtuous cycle where Cognitive DevOps tools accelerate the development of custom Salesforce applications, which in turn creates greater demand for advanced AI management services.

Why These Numbers Matter

The implications are profound:

Cost Efficiency: The 40%-60% VE discount underscores meaningful potential cost reductions for customers, positioning AI-native service providers to disrupt traditional providers significantly.

Competitive Shifts: GSIs and consultancies that don’t adopt Cognitive DevOps could lose substantial market share by 2030, as customers shift toward more automated, efficient providers. Cognitive Commoditization forces traditional consultancies to confront what we’ve called the New Intelligence Gradient.

Accelerated Salesforce Adoption: Lower implementation and operational costs enabled by VEs could boost Salesforce’s own platform growth by making broader deployments economically attractive.

What’s Next?

Despite our conservative adoption projections, the broader market implications remain profound. The 20x disparity between software and services markets signals a fundamental transformation in how enterprise services are delivered and consumed.

For investors and enterprise strategists, the key takeaway isn’t the specific dollar figure but the directional shift: AI-powered virtual employees are poised to fundamentally alter the economics of enterprise service delivery, regardless of whether adoption reaches 9% or exceeds 20% by decade’s end.

Stay tuned for our follow-up, where we’ll dive deeper into market dynamics, tackle that elusive VE TAM question, and explore more granular factors influencing VE adoption rates and vendor competition.

Cognitive DevOps Players to Watch

Here’s a snapshot of key vendors in this emerging space:

- SRE.ai – A Y Combinator–backed startup delivering AI-driven Salesforce DevOps agents that let teams deploy changes and configure workflows through natural-language prompts and best-practice templates, reducing manual clicks and release headaches.

- Cirra AI – An early-stage platform introducing “Change Agent” admin bots that interpret plain-English org clean-up or configuration requests and autonomously execute metadata changes (with human approvals as needed).

- Ressl AI – A toolset acting as virtual Salesforce admins: it scans org metadata for technical debt, generates refactoring plans, and uses multi-agent automation to implement changes up to 10× faster, all while maintaining compliance and documentation.

- Cloobot – Backed by Alchemist Accelerator, this vendor offers an AI co-pilot for Salesforce architects: a multi-agent system that monitors deployments, diagnoses issues (like merge conflicts), and auto-remediates them, speeding implementation by roughly 4x.

- TestZeus—Crafting a GenAI QA copilot that auto-writes, runs, and self‑heals test cases across all Salesforce clouds.

- Hubbl Technologies – A DevOps workbench that pairs process intelligence with AI copilots; for example, with an org analysis it can suggest org changes and send requests to Swantide for autonomous implementation.

- Swantide – A platform delivering “Admin-as-a-Service” for RevOps teams by translating sales ops change requests into instant Salesforce configuration updates, using workflow templates and an AI assistant to apply best practices and document every change.

- Sweep – A point-and-click release automation tool for complex Salesforce orgs that uses an AI engine to map out dependencies and even prepare rollback plans, so admins can deploy updates faster and revert safely if something goes wrong.

- Synch – A Canadian startup building a Git-centric Salesforce DevOps pipeline that uses AI agents to keep sandboxes and orgs in sync (eliminating drift) and to automatically flag risky commits, bringing modern source-control practices to Salesforce development.

- Elements.cloud – A metadata intelligence suite that now leverages AI for change analysis: it can generate impact assessments for proposed changes and recommend refactoring steps, helping teams proactively manage technical debt before deployment.

- Copado – A leading Salesforce DevOps platform has embedded a generative AI assistant (Copado AI Companion) that helps dev teams with everything from auto-generating test cases and refining user stories to running compliance checks and suggesting optimal deployment steps in their CI/CD pipeline.

- Opsera – A DevOps orchestration platform that now includes Hummingbird AI to unify toolchains: it automates CI/CD pipelines across any stack and provides predictive insights (like DORA and quality metrics enhanced by AI) at each stage, helping enterprises release faster with end-to-end visibility.

- Testsigma – A low-code test automation provider that recently integrated generative AI to auto-create and maintain Salesforce test suites: its AI can propose new end-to-end test steps, self-heal tests when configurations change, and run comprehensive regressions with minimal human input.

- AuctorAI – A Y-Combinator venture from the current batch developing cognitive DevOps agents helping with pre-sales requirements development.